The core problem most lenders face isn't a lack of effort. It's targeting the wrong businesses, using inconsistent outreach, and skipping qualification entirely. The result: high activity, low conversion, and a pipeline full of names that go nowhere.

This guide covers how to define a quality lead, a step-by-step framework for finding commercial lending leads across proven channels, what to set up before you start, the variables that most affect results, and the mistakes that quietly drain your pipeline.

Key Takeaways

- A commercial lending lead needs a financing need, decision-making authority, and a business profile that fits your loan product — qualify on all three

- Effective lead generation combines LinkedIn, cold email, phone, and referrals; no single channel carries the full load

- Lead quality depends on a clearly defined ICP, consistent qualification, and structured follow-up

- Before launching outreach, you need clean data, a CRM, a documented ICP, and basic compliance awareness

- If building an in-house pipeline is too time-consuming, outsourcing to a verified appointment-setting partner is a faster path to ROI

What Makes a Commercial Lending Lead Worth Pursuing?

Not every business contact qualifies as a lead worth your time. Three conditions need to align before a prospect deserves focused attention:

- A legitimate, timely financing need — not theoretical interest, but an active or near-future capital requirement

- Authority or influence to act — the contact can make or meaningfully influence the borrowing decision

- A financial profile that fits your product — loan size, business type, and creditworthiness align with what you actually offer

When any one of these is missing, you're investing outreach effort in a contact who can't convert.

New Financing vs. Refinancing Leads

These two categories require different outreach angles entirely:

- New financing — businesses seeking capital for expansion, acquisition, equipment, or working capital; the value proposition centers on enabling growth

- Refinancing — existing borrowers looking to restructure debt or access equity; the value proposition centers on better terms, cash flow relief, or consolidation

Lead Stages That Matter for Prioritization

| Stage | Definition | Right Action |

|---|---|---|

| IQL | Showed interest, no meaningful engagement | Nurture with content, not a sales call |

| MQL | Responded to a campaign or content | Follow-up sequence with light qualification |

| SQL | Confirmed authority, need, and timeline | Direct, focused outreach — book the meeting |

Characteristics of a High-Quality Lead

- Relevant industry or business type for your loan product

- Loan size that fits within your parameters

- Decision-maker title: owner, CFO, or controller

- A trigger event: lease expiration, equipment purchase, expansion announcement, or ownership change

The data backs up prioritizing quality over volume. According to Demandbase's 2026 State of ABM benchmark, organizations targeting buyers based on precise account criteria achieve 2–3x higher win rates than those using broad, lead-centric models. A short list of well-qualified SQLs will consistently outperform a large, loosely filtered contact list.

How to Find Commercial Lending Leads: A Step-by-Step Framework

Finding commercial lending leads is not a single action. It's a repeatable system that compounds over time. Here's how to build it.

Step 1: Define Your Ideal Client Profile (ICP)

Your ICP for commercial lending should document:

- Industry vertical — manufacturing, healthcare, real estate, professional services

- Business size — revenue range or employee count

- Geography — state, metro area, or regional market

- Loan type — SBA, equipment finance, commercial real estate, working capital

- Trigger events — what signals readiness to borrow (lease renewal, new hire surge, acquisition plan)

Skipping this step is the single most common reason outreach fails. Without a defined ICP, you can't segment your list, personalize messaging, or measure what's working.

TopLead builds data-backed ICP frameworks during onboarding, using firmographic criteria, intent signals, and historical client data — a practical model whether you're building this capability in-house or outsourcing it.

Step 2: Build a Targeted Prospect List

Primary data sources for commercial lending prospecting:

- LinkedIn Sales Navigator — filter by title (CFO, owner, controller), company size, and industry

- SBA databases and public business registries — useful for identifying businesses that have previously accessed capital

- County recorder and assessor records — valuable for property-based financing leads

- Industry association directories — often segmented by vertical and company size

Buying pre-made lists vs. building from primary sources:

Pre-made lists are faster but typically suffer from outdated data. According to Validity's 2025 State of CRM Data Management report, 76% of CRM users say less than half of their organization's data is accurate and complete. Purchased lists are rarely cleaner. Building from primary sources takes more time but produces contact data that actually reaches the right decision-maker.

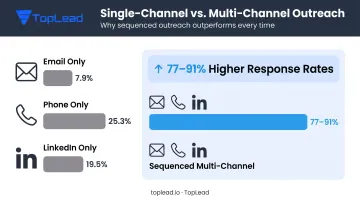

Step 3: Launch Multi-Channel Outreach

No single channel is sufficient. Multi-channel outbound cadences increase response rates by 77–91% compared to single-channel approaches, according to Salesloft's cadence research.

Channel-specific guidance:

- Cold email — keep it short, personalize to a trigger event, lead with value rather than your product. Tuesday through Thursday mornings tend to produce the highest engagement for B2B outreach

- LinkedIn — most effective for warming a contact before you call; connect, engage with their content, then reach out directly

- Phone — most productive after at least one prior digital touchpoint; cold calling a completely cold contact is significantly less effective than calling someone who's already seen your name

TopLead's financial services campaigns use all three channels in coordinated sequences, which reflects the same principle: the combination matters more than any individual channel.

Step 4: Qualify Every Lead

Apply this framework before investing significant sales time:

- Does the business have an active or near-future financing need?

- Does your contact have decision-making authority — or direct influence over who does?

- Does the loan type and size align with your product?

Leads that fail on any of these points should be deprioritized, not abandoned entirely. Some will become SQLs in 3–6 months with light nurturing.

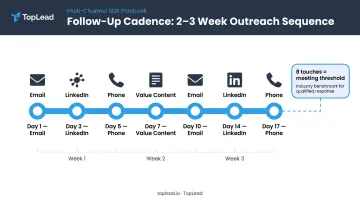

Step 5: Nurture and Follow Up Systematically

Most commercial lending leads don't convert on first contact. RAIN Group's research with 488 buyers and 489 sellers found it takes an average of 8 touches to generate a meeting with a new prospect. Yet the same research shows the majority of sellers stop well before that.

A structured follow-up cadence should include:

- Minimum 5–7 touchpoints over 2–3 weeks

- A mix of email, phone, and LinkedIn messages

- Value-add content between pitches: market rate updates, lending guides, or relevant news about their industry

Ad-hoc follow-up is not a cadence. Without a defined sequence, most leads go cold before you've reached the threshold where they'd actually respond.

What You Need Before Launching Outreach

Lenders who launch outreach without the right infrastructure tend to burn through lists, miss follow-ups, and leave a weak impression on prospects who won't give a second chance. Getting three things in order first — your ICP, your CRM, and compliance awareness — prevents most of those problems.

ICP and Segmentation Data

Your ICP needs to be documented before any outreach begins. Without it, you can't segment your list, write relevant messaging, or measure which targeting criteria actually produce qualified leads.

CRM and Tracking Tools

A CRM is essential — tracks lead status, manages follow-up sequences, and captures meeting outcomes so nothing falls through. Common options include HubSpot, Salesforce, Pipedrive, and Close.io — TopLead integrates with all of these when delivering appointments to clients, which means incoming meetings land directly in your existing workflow.

Compliance Awareness

Commercial lending outreach sits inside financial services regulations. Before launching:

- Verify that your contact lists are sourced legally

- Ensure email campaigns comply with CAN-SPAM (and CASL if you're reaching Canadian businesses)

- Review any claims in outreach materials for accuracy — vague or misleading statements about loan terms create regulatory exposure

If a lead generation vendor doesn't raise compliance in the first conversation, treat that as a disqualifier — not a detail to sort out later.

Key Variables That Affect Lead Quality and Conversion

Two lenders using identical channels can get dramatically different results. These variables explain why.

Targeting Specificity

The narrower and more accurate your targeting, the higher the percentage of prospects who actually need your product. Targeting by industry vertical, loan type, and company size consistently produces better qualification rates than generic "businesses with revenue over $1M" criteria.

Connecting with six or more stakeholders within a target account produces a 34% lift in win rates, according to RAIN Group — which means precision targeting isn't just about finding the right company, it's about reaching the right people inside it.

Messaging Relevance and Personalization

Commercial borrowers are decision-makers who receive frequent outreach. Generic messages get ignored. Messages that reference a specific trigger — a recent expansion, equipment purchase, or lease coming up for renewal — get attention.

RAIN Group's research found that 67% of buyers are influenced by content customized specifically to their situation. Top-performing prospectors set 2.7x more meetings than average sellers, and the differentiator is their ability to deliver targeted, value-focused first contacts.

Channel Selection and Timing

Different decision-makers respond to different channels:

- Small business owners tend to respond to direct phone and email

- CFOs at mid-market firms often engage first on LinkedIn

- Tuesday through Thursday mornings are the highest-response windows for B2B outreach

A sequenced multi-channel cadence outperforms single-channel outreach in every comparison. Multiple independent studies on B2B sales sequencing reach the same conclusion.

Lead Qualification Rigor

Verifying decision-maker authority and financing readiness before booking a meeting directly shortens sales cycles. Unqualified leads don't just fail to convert — they distort pipeline forecasting and consume follow-up capacity that should go to genuine SQLs.

Rigorous qualification is where the ROI compounds. TopLead's process for financial services appointments confirms authority level, financing need, and prospect fit before anything reaches a client's calendar. Sales teams spend time with prospects who can actually move forward — not contacts requiring three more screening calls before a real conversation starts.

Common Mistakes That Kill Your Commercial Lending Pipeline

Three patterns consistently undermine commercial lending pipelines — and all three are fixable:

- Chasing volume over qualification. Purchasing large, unfiltered lead lists produces high activity but low conversion. Every hour spent chasing an unqualified prospect is an hour not spent on a real opportunity.

- Relying on a single channel. Email-only or networking-only outreach creates a fragile pipeline. When that channel underperforms — due to inbox fatigue, algorithm changes, or low event attendance — everything stalls at once.

- Skipping structured follow-up. Most commercial lending prospects aren't ready to act on initial outreach. Without a consistent cadence, the majority of your marketing investment gets abandoned before it can convert. Research suggests most B2B sales require 6–8 touches; stopping at three means leaving qualified prospects on the table.

When to Build In-House vs. Outsource Commercial Lending Lead Generation

This is a resource allocation question. Both approaches work — the right choice depends on team capacity, speed-to-pipeline requirements, and cost efficiency.

When Building In-House Makes Sense

In-house lead generation works well when your team has:

- Dedicated SDR capacity with clear ownership of the prospecting function

- A documented ICP and established outreach tools

- Enough time to run, test, and optimize multi-channel campaigns

- The infrastructure to manage compliance, data sourcing, and CRM tracking

The benefit is full control over messaging and direct ownership of pipeline data.

When Outsourcing Delivers Faster ROI

Outsourcing makes sense when your sales team needs to focus on closing rather than prospecting, when you need to scale without adding headcount, or when internal attempts have produced inconsistent results.

TopLead's financial services appointment-setting program targets CFOs, controllers, business owners, and finance leaders across commercial banking, business lending, equipment finance, and capital advisory. Key program terms:

- Pay-per-appointment pricing at $300–$350 per qualified meeting

- Guaranteed minimum of 4–6 qualified appointments per month

- Reschedule or replacement guarantee if a prospect cancels

- 25,000+ appointments delivered across 15+ years in market

Every meeting is a verified decision-maker, booked directly to your calendar — no prospecting overhead required.

Hybrid Approach

Many commercial lenders use a hybrid model: outsourcing cold outreach and appointment setting to a specialist while keeping relationship-based channels — referral networks, industry events, and existing client cross-sell — managed internally. This balances cost efficiency with brand control.

Frequently Asked Questions

What are the 4 C's of commercial lending?

The 4 C's are Character (creditworthiness and track record), Capacity (ability to repay), Capital (the borrower's own financial resources), and Collateral (assets securing the loan). Understanding these helps lenders quickly assess which leads are likely to qualify before investing significant sales time.

How much should you pay for lead generation?

Costs vary by method. Content and SEO require time more than budget; paid ads scale with competition. Outsourced appointment-setting services charge per qualified meeting — typically a few hundred to over a thousand dollars depending on market complexity. TopLead's financial services appointments average $300–$350 per verified meeting.

What is a qualified commercial lending lead?

A qualified lead is a business contact with a confirmed financing need, the authority to make or influence borrowing decisions, and a business profile that fits the lender's loan product. All three criteria must be present.

What is the most effective channel for commercial lending lead generation?

Referral networks consistently produce the highest-quality leads, while LinkedIn and cold email work well at scale with strong targeting. A sequenced multi-channel approach — combining all three — outperforms any single channel used in isolation.

How do you convert commercial lending leads into clients?

Conversion depends on a structured follow-up cadence and messaging tied to the prospect's specific financing trigger. Most commercial leads need multiple touchpoints — consistency and timing matter more than any single outreach attempt.

Should I buy commercial lending leads or generate them organically?

Purchased lists offer speed but typically suffer from outdated data and low qualification rates. Organically generated leads — through referrals, targeted outreach, and content — convert at higher rates. A blended approach using verified data sources alongside structured outbound outreach delivers the best combination of volume and quality.