Introduction

Financial services firms face a lead qualification problem that most B2B industries don't. A prospect downloading a whitepaper might be a CIO actively evaluating managers — or a compliance officer gathering background on competitor products. Without a structured way to tell them apart, relationship managers burn time chasing researchers while genuine buyers go cold.

The gap is costly. A generic scoring model won't fix it. Standard B2B frameworks assume short sales cycles, single decision-makers, and low switching costs. Financial services violates all three.

This guide covers what lead scoring actually means in a financial services context, why off-the-shelf models misfire, and how to build a four-dimension scoring model that accounts for AUM thresholds, buying committees, and compliance timelines. It also walks through how to connect that model to a handoff process that sales teams will actually use.

Key Takeaways

- Generic B2B lead scoring fails in financial services because it ignores compliance review periods, multi-stakeholder buying committees, and the depth of firmographic data required

- Effective models combine four dimensions: firmographic fit, role-based authority, behavioral intent, and negative scoring

- 68% of marketers using intent and behavior data alongside ICP alignment report higher account win rates (Demand Gen Report)

- MQL-to-SQL handoffs require written qualification criteria that both sales and marketing have explicitly agreed upon

- Models must be calibrated against closed-won data and reviewed quarterly to stay accurate

What Is Lead Scoring in Financial Services (and Why Generic Models Fall Short)

Lead scoring in financial services assigns numeric values to prospect attributes — firmographic fit, AUM range, regulatory registration, role seniority — and to behaviors like meeting requests, DDQ downloads, and pricing page visits. The composite score tells relationship managers which prospects deserve immediate outreach and which need continued nurturing.

The problem: standard B2B scoring frameworks weren't built for this environment.

Three Assumptions Generic Models Get Wrong

Most scoring tools assume:

- A 30–90 day sales cycle — Institutional due diligence alone typically takes approximately 3–6 months per Nasdaq, before factoring in committee review, legal, and board approval

- A single decision-maker — Retirement plan committees typically range from 3–7 members, with 5 described as ideal, per TIAA's research on defined contribution governance

- Low switching costs — In financial services, regulatory exposure, fiduciary liability, and reputational risk make prospects extremely deliberate. Switching isn't a tactical decision

Where Off-the-Shelf Models Break Down

Off-the-shelf frameworks misfire in predictable ways once financial services realities enter the picture:

- Time decay settings punish silence during compliance review. A lead that goes quiet for 60 days isn't cold — it may be in internal legal review. Penalizing that inactivity drops legitimate prospects out of scoring queues

- Content engagement gets overweighted. A compliance officer downloading a whitepaper for regulatory review looks identical to a CIO building a manager shortlist. Generic models treat both as buying signals

- Firmographic data is too shallow. Knowing a prospect is in "financial services" is nearly useless. You need AUM range, firm type (RIA vs. broker-dealer vs. family office), registration status, and custodial platform

Rule-Based vs. Predictive Models

Understanding where generic models fail points directly to which model type makes sense at your stage. Most financial firms start with rule-based scoring — marketing manually assigns point values based on observed patterns. Once 50–100 closed-won deals accumulate, predictive models using machine learning can identify subtler conversion patterns in historical data.

Rule-based is the right starting point. Move to predictive once your closed-deal history is deep enough to train on — rushing that transition before the data is there produces models that reflect noise, not signal.

The Four Dimensions of a Financial Services Lead Scoring Model

No single data point reliably predicts conversion in financial services. Effective models require four dimensions working together, weighted against the firm's own historical conversion data — not a generic template.

Firmographic Scoring: Who Is the Organization?

Firmographic scoring determines whether the prospect's firm matches your ideal client profile before any behavioral signal matters.

Common firmographic scoring criteria:

- AUM range — An alternatives asset manager scores accredited investor status heavily; a 401(k) advisor weights plan assets and participant count

- Firm type — RIA, broker-dealer, family office, pension fund, endowment, OCIO each carry different buying processes and authority structures

- Regulatory registration — SEC-registered vs. state-registered vs. non-registered carries different compliance implications and engagement timelines

- Custodial platform — Schwab, Fidelity, or Pershing custodians often signal firm size and product compatibility

- Number of advisors — Relevant for practice management tools and group benefits programs

Worth noting for distribution-focused firms: Cerulli's 2025 institutional distribution research found the top five investment consulting providers advise on 70% of worldwide assets. If your distribution depends on consultants or OCIOs as gatekeepers, firmographic scoring must account for those intermediaries — not just direct prospects.

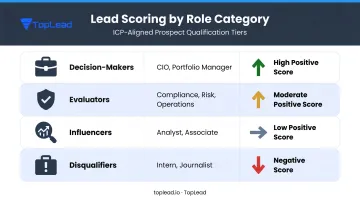

Role-Based Scoring: Who Is the Individual?

Not every contact at a target firm carries equal buying authority. Assign points accordingly:

| Role Category | Examples | Score Direction |

|---|---|---|

| Decision-makers | CIO, Portfolio Manager, Director of Research, Managing Partner | High positive |

| Evaluators | Operations, Compliance, Risk | Moderate positive |

| Influencers | Analyst, Associate | Low positive |

| Disqualifiers | Intern, Student, Journalist | Negative |

Without role scoring, a firm can accumulate high composite scores from contacts who cannot approve a mandate.

Behavioral Scoring: What Has the Prospect Done?

Behavioral signals indicate intent — but only when weighted by how closely each action correlates with pipeline generation, not by how easy each action is to track.

High-intent signals (weight heavily):

- Meeting request or demo booking

- DDQ (due diligence questionnaire) or RFP download

- Repeated visits to performance or pricing pages within a short window

- Responding to outreach with specific questions

Low-intent signals tell a different story and should be weighted minimally:

Low-intent signals:

- Opening a single email

- Reading one blog post

- Attending a general-topic webinar

A model where a meeting request scores the same as five email opens will surface false positives constantly.

Negative Scoring: Eliminating False Positives

Negative scoring is what makes a model trustworthy. Without it, scores inflate with competitors, journalists, and job seekers.

Apply negative values to:

- Competitor email domains

- Personal email addresses (Gmail, Yahoo) for institutional-targeted programs

- No engagement for 90+ days

- Unsubscribe action

- Job titles indicating student or press roles

A financial services-specific exception: compliance officer interactions should generally be excluded from behavioral scoring unless they occur alongside buying signals from other contacts at the same account. A compliance officer downloading materials is often regulatory due diligence, not a purchase signal.

How to Build Your Financial Services Lead Scoring Model

Step 1: Start with Closed-Won Data

The most reliable starting point is your own historical data, not an industry template.

Pull 50–100 closed-won deals and map:

- Firmographic attributes present at the time of first engagement

- Contact roles that appeared in the buying process

- Behavioral signals that preceded each close and at what frequency

These patterns become the empirical basis for point value assignments. Firms lacking sufficient closed-won data can use industry conversion benchmarks as a temporary proxy, then recalibrate as their own data accumulates.

Step 2: Define Your Ideal Client Profile

The ICP for financial services must go deeper than standard B2B definitions. It should specify:

- AUM range or plan asset size

- Firm type and regulatory registration

- Geography and state-specific licensing relevance

- Technology stack (CRM, custodial platform)

- Decision-maker title and committee structure

- Trigger events that precede buying decisions: hiring a new CIO, launching a new product, approaching a plan renewal date, or reaching a regulatory milestone

Sales and marketing must co-create the ICP. Scoring models built by marketing alone consistently produce leads that sales rejects.

Step 3: Assign Point Values Using Conversion Rate Analysis

For each scoring attribute, calculate what percentage of historical leads with that attribute converted to clients. Compare it to your overall baseline conversion rate. Assign higher points to attributes where the conversion rate meaningfully exceeds the baseline.

For example, if leads from RIAs with $500M+ AUM converted at a rate materially higher than your baseline, that combination earns proportionally higher points. Use your own closed-won data for these figures — generic benchmarks produce a model that reflects someone else's buyers, not yours.

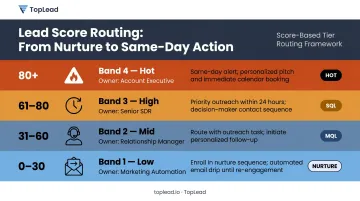

Step 4: Set Thresholds and Automate CRM Routing

Once point values are set, define thresholds that trigger automated actions:

| Score Range | Action | Owner |

|---|---|---|

| Low (e.g., 0–30) | Add to nurture sequence | Marketing automation |

| Mid (e.g., 31–60) | Route to relationship manager with outreach task | Sales (MQL) |

| High (e.g., 61–80) | Priority outreach within 24 hours | Sales (SQL) |

| Hot (e.g., 80+) | Same-day alert, prepare personalized pitch | Sales (urgent) |

Without CRM automation, scores remain a data exercise. They don't change behavior.

That automation gap is most acute for firms still accumulating the closed-won data their model needs to mature. During that period, outbound appointment-setting services like TopLead can directly supplement the pipeline.

TopLead delivers pre-qualified appointments with verified decision-makers, confirmed against firmographic and role-based criteria including AUM thresholds, firm type, and trigger events, directly into the client's CRM via Salesforce, HubSpot, Pipedrive, and other major platforms. Each appointment arrives with qualification notes, so relationship managers walk into conversations already knowing the prospect's authority level, pain points, and stated timeline. With clients including Edward Jones, UBS, Wells Fargo Advisors, and LPL Financial, and 25,000+ appointments arranged, TopLead provides consistent SQL volume while the internal scoring model builds its dataset.

MQL vs. SQL: Defining the Handoff That Closes More Deals

Defining Each Stage for Financial Services

MQL (Marketing Qualified Lead): Has met minimum demographic and behavioral thresholds. Fits the target firm profile and has engaged with multiple content assets. Has not yet shown explicit purchase intent.

SQL (Sales Qualified Lead): Has taken actions indicating active evaluation — requesting a meeting, asking for a DDQ, engaging with performance or pricing content in a pattern consistent with active review — and has been accepted by the sales team as ready for direct outreach.

The distinction matters more in financial services than in most B2B categories because the cost of a false positive is high. Relationship managers who receive unqualified leads stop trusting the scoring model entirely.

Closing the MQL-to-SQL Gap

The gap between MQL and SQL is where most financial firms lose pipeline. Marketing generates leads that technically meet scoring thresholds; sales rejects them because the qualification criteria don't reflect what a relationship manager actually needs for a productive conversation.

Closing this gap requires both teams to agree in writing on what "qualified" means before the scoring model is built. Aberdeen research found that organizations with aligned sales and marketing functions achieved 20% average annual revenue growth, compared to a 4% average decline among those without alignment — a gap that holds across industries.

Adjusting Time-Decay for Long Buying Cycles

Standard CRM time-decay settings penalize leads for 30–60 days of inactivity. In financial services, that's a compliance review window, not disengagement.

Adjust decay settings to reflect your actual sales cycle. More useful than recency alone: engagement velocity — the frequency of interactions over a set window. A prospect who engages three times in a month after six weeks of silence is more valuable than recency alone suggests.

Maintaining Handoff Quality Over Time

Scoring models degrade without feedback. Sales teams must report monthly on which scored leads converted and which were false positives — that input is what allows the model to improve quarter over quarter.

Most firms stall at this step because relationship managers prioritize client work over CRM data entry. The feedback loop only functions when leadership ties it directly to pipeline forecasting and holds teams accountable for completing it. Without that mandate, scoring accuracy erodes within two quarters.

For the loop to hold, three things need to be in place:

- A standardized disposition field in the CRM (converted, rejected, or recycled)

- Monthly review cadence between sales and marketing leadership

- Score recalibration tied to actual close data, not just MQL volume

Common Lead Scoring Mistakes Financial Firms Make

Three patterns consistently undermine lead scoring in financial services. Avoid all of them.

1. Scoring Activity Instead of Intent

Opening an email is activity. Clicking through to a performance attribution page and returning twice in one week is intent. Many firms over-weight email opens and blog visits, which rewards anyone with a functioning inbox.

High-intent actions (meeting requests, DDQ downloads) should always meaningfully outscore passive engagement. That calibration should be validated against closed-won patterns, not assumed.

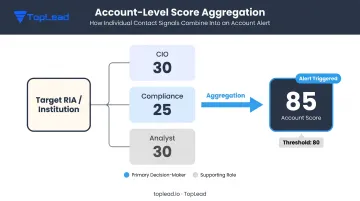

2. Ignoring Account-Level Scoring

In financial services, the buying unit is the firm, not the individual. If three contacts from the same RIA each score 30 points separately, the account-level signal is far stronger than any individual record suggests.

Cerulli's data on consultant concentration reinforces this: in institutional distribution, influence is often spread across multiple contacts and intermediaries at the same organization. Aggregate contact scores within accounts and use that aggregate to trigger account-level alerts.

3. Building Once, Reviewing Never

Two failure modes tend to arrive together: the model is built once and left untouched as buyer behavior evolves, and sales and marketing never formally agreed on what "qualified" means in the first place.

Fix both at the same time. A quarterly model review cadence and a written MQL/SQL definition document, signed off by both teams, are the minimum requirements to keep a scoring model functional.

Frequently Asked Questions

How do you calculate lead scoring?

Assign point values to prospect attributes (firmographic fit, job role) and behaviors (meeting requests, DDQ downloads), then sum those values into a composite score. In financial services, weights should be derived from historical closed-won data, comparing conversion rates by attribute against your overall baseline conversion rate.

What are lead scoring criteria?

Criteria are the specific attributes and actions used to assign points. For financial services, they span four categories: firmographic fit (AUM, firm type, registration status), role-based authority, behavioral signals (DDQ requests, meeting requests), and negative disqualifiers (competitor domain, personal email, prolonged inactivity).

What is an example of lead scoring in financial services?

A prospect at an RIA with $750M AUM (+20 pts), where the contact is the CIO (+25 pts), downloaded a due diligence questionnaire (+25 pts), and requested a meeting (+30 pts) reaches a composite score of 100 — well above a typical SQL threshold of 70, triggering immediate relationship manager outreach.

What is the difference between MQL and SQL in financial services?

An MQL has met minimum fit and engagement thresholds (downloaded content, attended webinars) but hasn't shown explicit purchase intent. An SQL has demonstrated active evaluation behavior, such as requesting a meeting or stating a specific allocation timeline, and the sales team has accepted them for direct outreach.

How often should a financial firm update its lead scoring model?

Quarterly reviews are standard. Compare scores of leads that closed versus went cold, then adjust point values where the model misjudged. Major market events, such as interest rate shifts or regulatory changes, may warrant an off-cycle recalibration.

Can smaller financial firms implement lead scoring without expensive software?

Yes. Start with a spreadsheet-based scoring matrix and manual weekly review. Free or low-cost CRM tiers provide basic automation. Defining clear qualification criteria and aligning sales and marketing on those definitions matters far more than the sophistication of the software you use.