Introduction

Insurance is one of the most competitive B2B service categories in the country. With 39,000 independent P&C agencies operating across the U.S. and over 338,000 insurance sales agents competing for the same commercial accounts, standing out requires more than a good product and a referral network.

The challenge is pipeline, not awareness. Most agencies are familiar with the channels—SEO, PPC, LinkedIn, email, cold outreach—but execution is where results diverge. Which channels you prioritize, how precisely you define your target audience, and whether your tactics reinforce each other all determine whether a campaign produces revenue or just activity.

This guide breaks down the digital methods that produce results for insurance lead generation, how to sequence them into a working system, and the execution mistakes that kill ROI before a campaign builds momentum.

Key Takeaways

- Insurance pipelines require multiple channels working together — no single tactic sustains consistent lead flow

- The five core methods are SEO/content, PPC, LinkedIn/social, email nurturing, and cold outreach

- Lead quality outweighs lead volume: targeting precision and follow-up speed drive more revenue than a large contact list

- Contacting a lead within the first hour significantly improves your chances of reaching and qualifying them

- Agencies unable to scale internally can accelerate pipeline growth by outsourcing to a pay-per-appointment outbound partner

Core Digital Strategies for Generating Insurance Leads

Each digital method addresses a different stage of the buyer journey. Some produce immediate, high-intent leads. Others build long-term pipeline. Used together, they create a compounding system—used in isolation, they plateau quickly.

SEO and Content Marketing

Insurance buyers often begin with a search. Queries like "commercial general liability insurance for contractors" or "employee benefits broker for small businesses" signal active research, and agencies that own those rankings capture prospects before competitors enter the picture.

The SEO approach for insurance breaks into two tracks:

- Informational content — blog posts and FAQs targeting research-phase queries (e.g., "what does a BOP policy cover")

- Service pages — location-specific or coverage-specific landing pages targeting transactional queries (e.g., "workers comp insurance broker in Phoenix")

Local SEO deserves particular attention for independent agents and regional brokers. Optimizing your Google Business Profile, building consistent local citations, and creating location-specific landing pages captures prospects with geographic intent—a meaningful segment given that nearly a quarter of small business owners now research insurance online before making a decision.

The trade-off: SEO compounds over time but rarely produces leads in the first 90 days. It's a long-term investment that runs in the background while faster channels fill the immediate pipeline.

PPC Advertising (Google Ads)

Google Search Ads solve the timeline problem. When a CFO searches "commercial property insurance quote," a well-structured campaign puts your agency at the top of the results within days of launch—not months.

WordStream's 2025 Google Ads benchmarks for the Finance and Insurance category show:

| Metric | Finance & Insurance Benchmark |

|---|---|

| Click-through rate | 8.33% |

| Cost per click | $3.46 (category average) |

| Conversion rate | 2.55% |

| Cost per lead | $83.93 |

These are category-wide figures. Commercial insurance keywords—particularly workers' comp, general liability, and employee benefits—tend to run considerably higher due to competition and policy value. Budget expectations should reflect that reality.

What determines whether PPC converts or burns budget:

- Campaign structure — tight ad groups, precise match types, and aggressive negative keyword lists

- Landing page quality — specific, benefit-focused pages that match the ad's promise

- Offer clarity — a clear next step (quote request, consultation booking) above the fold

LinkedIn and Social Media Outreach

LinkedIn is the most direct path to B2B insurance decision-makers. With over 1 billion professionals on the platform, it lets employee benefits brokers and commercial lines agents filter by job title, company size, industry, and geography.

That targeting precision—reaching CFOs, HR directors, and business owners specifically—is something no other social channel matches.

Two LinkedIn approaches worth running in parallel:

- Organic outreach — connection requests and direct messaging to prospects matching your ICP, with messaging tied to specific triggers (renewal timing, growth events, compliance changes)

- LinkedIn Ads — sponsored content and InMail campaigns for broader awareness and retargeting

Facebook and Instagram serve a different function for insurance lead generation. They're not great for cold prospecting, but they're effective for retargeting—serving ads to prospects who visited your website but didn't convert, keeping your agency visible while they continue their evaluation.

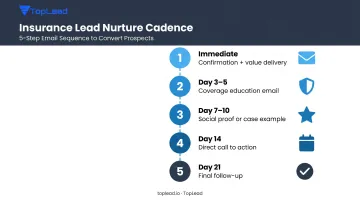

Email Marketing and Lead Nurturing

Most insurance leads don't convert on first contact. A quote-request form submission or guide download signals interest, not readiness—and without a structured follow-up sequence, that lead evaporates.

An effective email nurture cadence for insurance typically looks like:

- Immediate confirmation + value delivery (guide, checklist, or relevant resource)

- Coverage education email 3–5 days later (address a specific risk scenario relevant to their industry)

- Social proof or case example at day 7–10

- Direct call to action at day 14 (offer a consultation or coverage review)

- Final follow-up at day 21 before moving to a lower-frequency track

Segmentation determines whether your email program converts or generates unsubscribes. A manufacturing company approaching workers' comp renewal has nothing in common with a 75-person tech firm evaluating employee benefits. Mailchimp's benchmark data shows insurance emails average a 20.68% open rate and 2.45% click-through rate—segmented lists consistently outperform those averages; unsegmented lists fall below them.

Cold Outreach (Cold Email and Cold Calling)

For commercial insurance brokers targeting specific industries or company sizes, outbound cold outreach remains one of the fastest ways to generate pipeline. You control who you reach, when you reach them, and how you position the conversation.

Four factors determine whether cold outreach builds pipeline or wastes effort:

- A well-defined ICP — targeting by industry, employee count, geography, and trigger event (not "any business that needs insurance")

- Verified contact data — current, validated contacts for the right decision-makers at target companies

- Trigger-based messaging — outreach tied to renewal windows, mod rate spikes, premium audit shocks, or headcount growth rather than generic pitches

- Multi-touch follow-up — a structured cadence across email, phone, and LinkedIn rather than a single message and silence

Cold email benchmarks from Woodpecker's dataset show approximately 53% average open rates for targeted sequences, with reply rates around 3.4% on average and top-performing campaigns reaching 10%+. The campaigns that hit 10%+ share one trait: messaging tied to a specific trigger, not a generic pitch.

Building a Multi-Channel Insurance Lead Generation Cadence

Channels running in isolation produce inconsistent results. Agencies that generate predictable pipeline treat their outreach as a coordinated sequence — where each touchpoint builds on the last and the prospect experiences a single coherent conversation, not a series of disconnected messages.

Step 1: Define Your ICP and Segment Your Target List

Before launching any channel, define exactly who you're trying to reach. Vague profiles ("any manufacturer" or "small businesses in the Midwest") produce weak lists and wasted spend.

A strong ICP for commercial insurance includes:

- Industry and SIC code — construction, healthcare, transportation, etc.

- Employee headcount — small group (2–50), mid-market (51–500), or larger

- Geography — state or metro area, particularly relevant for workers' comp in monopolistic states

- Trigger signals — approaching renewal, recent premium spike, mod rate increase, recent hiring surge

For group health campaigns, the ICP typically targets companies 50–200 employees in growth industries. For workers' comp, the focus shifts to high-exposure industries where mod rates are actively managed.

Step 2: Set Up Tracking Infrastructure Before Launch

CRM integration, UTM parameters, call tracking, and lead source tagging must be configured before the first email goes out. Skipping this step makes it impossible to know what's working—and in a multi-channel environment, attribution is everything.

Minimum tracking setup:

- CRM with lead source fields (channel, campaign, date)

- UTM parameters on all paid and email links

- Call tracking numbers for phone-specific attribution

- Monthly pipeline review connecting lead source to closed revenue

Step 3: Sequence Multi-Channel Touchpoints Over a Defined Window

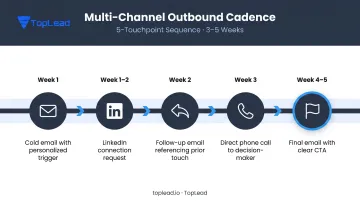

A typical 3–5 week outbound cadence for commercial insurance:

- Week 1 — Initial cold email (trigger-based, specific to their industry or renewal timing)

- Week 1–2 — LinkedIn connection request with a brief, relevant note

- Week 2 — Follow-up email referencing the first message

- Week 3 — Phone call with context from prior emails

- Week 4–5 — Final email with a clear next step or opt-out offer

Each touchpoint references the previous one, so the prospect sees a single thread rather than separate attempts to get their attention.

Step 4: Qualify Leads Before Routing to Sales

Not every response is a sales-ready lead. A basic qualification framework filters out poor fits before they consume a producer's time:

- Budget — Confirm they can afford the coverage or service you provide

- Authority — Verify you're speaking with the decision-maker: owner, CFO, or HR director

- Need — Identify a genuine coverage gap, renewal trigger, or broker dissatisfaction

- Timing — Determine when their current policy renews and how close the window is

Only prospects who clear all four criteria should be routed to a producer or senior broker for a consultation.

Key Variables That Affect Insurance Lead Quality

Volume metrics are easy to report. Conversion rates are what matter.

Response speed is one of the highest-leverage variables in insurance lead generation. Research from InsideSales shows that odds of contacting a lead drop by more than 10x within the first hour of inquiry, and qualification odds drop by more than 6x. Calling within 5 minutes versus 30 minutes produces 100x higher contact odds and 21x higher qualification odds.

For inbound leads—quote requests, guide downloads, contact form submissions—speed-to-response is often the difference between booking a meeting and losing the prospect to a competitor who called first.

Targeting precision determines lead quality at the top of the funnel. Two categories define most insurance lead sources:

- Shared leads — purchased from aggregators, distributed to multiple agents simultaneously. Lower cost, but the prospect is fielding calls from 3–5 competing brokers at the same time. Close rates reflect that.

- Exclusive leads — generated through owned channels (your SEO, your PPC, your outbound campaigns) or delivered exclusively through a direct outreach program. Higher cost per lead, but no competing agents in the picture.

The type of lead you generate also shapes how aggressively you need to follow up. Follow-up persistence closes more deals than any single touchpoint, and that's especially true in commercial insurance.

Decision-makers rarely change coverage on the first call. Renewal windows need to align, internal stakeholders need to weigh in, and trust takes time to build. A realistic B2B follow-up sequence looks like this:

- Day 1: Initial call or email within 5 minutes of inquiry

- Day 3: Second touchpoint referencing the original conversation

- Day 7–10: Value-add email (benchmark data, case study, or relevant guide)

- Day 14+: Check-in timed to renewal window or a recent trigger event

Common Mistakes That Kill Insurance Lead Generation ROI

Launching Broad Without a Defined ICP

Running Google Ads against generic keywords like "business insurance" or blasting cold emails to unverified, untargeted lists wastes budget and trains algorithms to optimize for the wrong signals. The fix is straightforward — but routinely skipped: define exactly who you're targeting before spending a dollar.

Your ICP should specify:

- Industry and sub-vertical

- Company size (headcount or revenue band)

- Geography

- Decision-maker title

- At least one trigger event that signals buying intent right now

Treating Lead Generation as a Campaign, Not a System

Insurance agencies frequently run a single campaign, exhaust a contact list, then stop when leads dry up. Restarting from scratch resets everything — list warmth, algorithmic optimization, pipeline momentum.

Consistent lead generation requires:

- Ongoing outreach that doesn't pause between campaigns

- Regular list refreshes with verified, current contacts

- Continuous content publishing to maintain inbound momentum

Agencies with predictable pipelines build lead generation into their operating rhythm as permanent infrastructure, not a quarterly push.

Ignoring Attribution and Channel ROI

If you don't know your cost per lead by channel, your cost per acquired client, and your close rate by lead source, you're flying without instruments. Many insurance agencies can tell you how many leads they got but not which channels produced the ones that closed.

At minimum, every agency should track:

- Lead source (channel and campaign)

- Cost per lead by channel

- Close rate by lead source

- Cost per acquired client by channel

Monthly pipeline reviews that tie marketing spend to revenue closed turn channel prioritization from guesswork into a data decision.

When to Build In-House vs. Partner with a Lead Generation Agency

Building internal lead generation capability—hiring SDRs, managing ad platforms, producing content, and maintaining CRM systems—is a real investment. It takes time to hire, train, and ramp a sales development team, and in the meantime, pipeline gaps compound.

The common pattern: an agency allocates part of a producer's time to prospecting, runs occasional ad campaigns, and sends periodic email blasts. None of these get enough consistent investment to produce consistent results. The agency concludes that "digital doesn't work for insurance" when the real issue was underinvestment across too many channels.

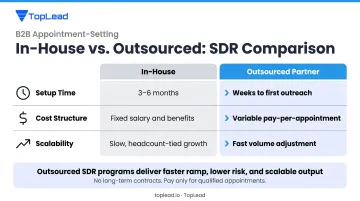

In-House vs. Outsourced: A Direct Comparison

| Dimension | In-House Build | Outsourced Partner |

|---|---|---|

| Setup time | 3–6 months to hire, train, and ramp | Weeks to first outreach |

| Cost structure | Fixed (salary, benefits, tools, management) | Variable (pay-per-appointment) |

| Scalability | Slow—tied to headcount | Fast—adjust volume without hiring |

Outsourcing makes the most sense when:

- An agency lacks dedicated sales development resources

- Verified decision-maker outreach at scale is needed quickly

- Compressing time-to-pipeline is the priority

A pay-per-appointment model like TopLead's removes the fixed cost risk of building an SDR team and guarantees a minimum number of qualified meetings each month.

TopLead's insurance programs run 3–6 months and deliver 4–6 qualified appointments per month at an average cost of $300–$350, with a reschedule or replacement guarantee on no-shows. Every appointment is verified for decision-maker authority (business owners, CFOs, HR directors, risk managers) before it lands on a producer's calendar.

Clients like Aflac, Hub International, AON, and Assured Partners have used this model to build commercial pipeline without rebuilding their internal teams first.

Outsourcing is an acceleration lever, not a substitute for owned digital assets. Agencies that invest in both—building long-term SEO and content while running outsourced outbound—consistently outperform those that choose one over the other.

Frequently Asked Questions

How do insurance lead companies get their leads?

Lead companies typically use a mix of owned websites optimized for search, paid ad networks, and partner site traffic to capture quote requests from consumers or businesses. Those requests are verified and distributed as either shared leads (sold to multiple agents simultaneously) or exclusive leads reserved for a single buyer.

Can ChatGPT do lead generation?

AI tools like ChatGPT can assist with lead generation tasks—drafting cold email sequences, generating SEO content, building prospect research workflows, and personalizing outreach at scale. They don't autonomously identify, contact, or qualify prospects without being integrated into a broader outreach system and CRM.

What is the best CRM for insurance agents?

Popular options include HubSpot, Salesforce, AgencyZoom, and HawkSoft. The right choice depends on whether the agency needs basic pipeline tracking, marketing automation, or insurance-specific features like policy management and renewal date tracking.

What is a good cost per lead for insurance?

It varies by channel and coverage line. The Finance and Insurance category average on Google Ads runs approximately $83.93 per lead. Qualified commercial insurance or employee benefits appointments generated through managed outbound programs typically run $300–$350 per appointment, reflecting the higher qualification standard and decision-maker verification involved.

How long does it take to see results from digital insurance lead generation?

Paid channels (PPC, LinkedIn Ads) can generate leads within days of launch. SEO and content marketing typically take 3–6 months to produce meaningful organic volume. A multi-channel approach balances short-term pipeline from paid and outbound with long-term compounding returns from organic channels.

What is the difference between shared and exclusive insurance leads?

Shared leads are sold to multiple agents at once, so the prospect fields calls from several competing brokers simultaneously. Exclusive leads go to a single agency through owned channels or direct outreach, arriving without competition and converting at higher rates.